Definition: Source Document is the root document that bears the essential information related to the business transaction. When a business transaction takes place, a piece of written, printed, typed or electronic trail is generated which stores data relating to the transaction and acts as a formal or official record. This document is the source document.

Basically, these documents substantiate the business transaction, whose entry is made in the books, as they are the first and foremost input to the accounting process.

Additionally, these documents carry a unique number, either numeric or alphanumeric, which not just helps in identification, but also facilitates referencing. And because these are pre-numbered, they help in the classification of transactions and also find out the missing source documents.

This documentary evidence contains the nature of the transaction, the name, and address of parties, date and amount of transaction, etc.

After recording the information provided by the source document, they are indexed and retained properly, to access them whenever required. In addition, the auditor can also review them at the time of auditing the company’s financial statement, to check whether the transactions have occurred in reality.

Think of a situation when we sell goods to customers, we prepare invoices for sending goods, bills receivable in case of credit sales, and cash memos in case of cash sales. The original is delivered to the customer, and the duplicate is retained as a record in the business. Such a duplicate copy is the source document.

Here, we are going to talk about some commonly used Source Documents:

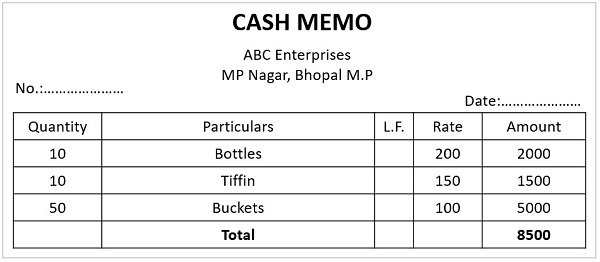

On purchasing goods in cash from a trader, the seller (trader) provides a cash memo to the buyer, as a receipt of purchase. It comprises the details of goods sold, i.e. name of selling organization, name of the purchaser, quantity, and price of the units purchased, date, and amount of the transaction, etc.

Specimen of Cash Memo

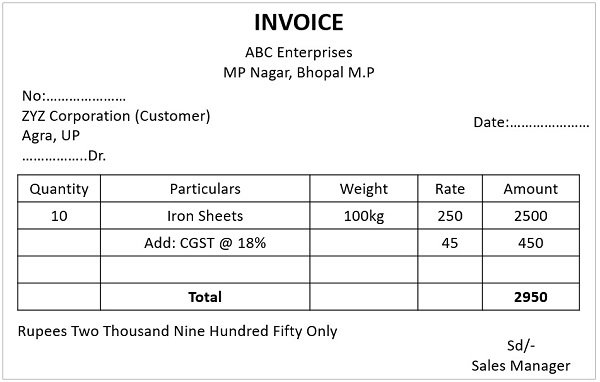

On the sale of goods on credit, the seller of the goods prepares a sales invoice. It is prepared in three copies, the first one is delivered to the buyer, the second one is kept in the bundle of goods, the third copy is retained by the seller for future reference. It contains the details like the name of the purchaser, description of goods sold, i.e. quantity and price of the units sold, total amount, and tax.

Specimen of Invoice

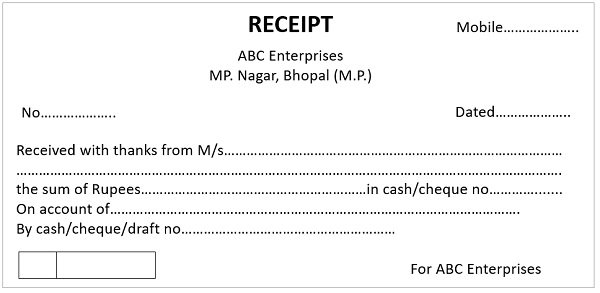

When a certain amount is received from a customer, a document is issued as a receipt that shows the date and amount of payment, details of the payer, and purpose of payment. The counterfoil or carbon copy of such receipt is used as a source document.

Specimen of Receipt

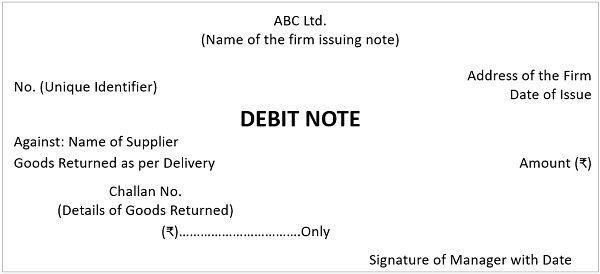

When the buyer of the goods returns them to the supplier, due to reasons like a defect, inferior quality, or substandard product. In such a case a note is given to the supplier along with the goods returned, which indicates that there is a debit in their account for goods given back to the supplier, which is called a debit note. It bears the date of return, quantity and amount, name of the supplier, and the reason for returning goods.

Specimen of Debit Note

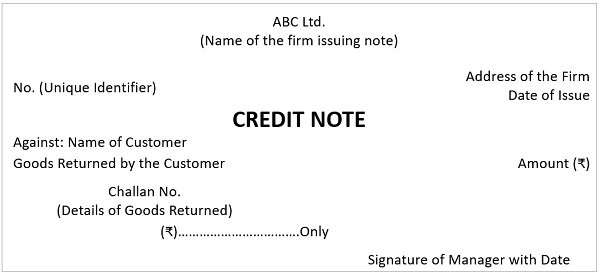

On receiving the goods returned by the customers for being defective or inferior in quality, along with a debit note, another note is issued by the seller to the purchaser, which indicates the acceptance of the claim raised by the purchaser, which is known as a credit note.

By issuing a credit note to the customer, the seller gives his affirmation regarding the acceptance of the goods as well as certifies that due credit will be provided for the goods returned.

Specimen of Credit Note

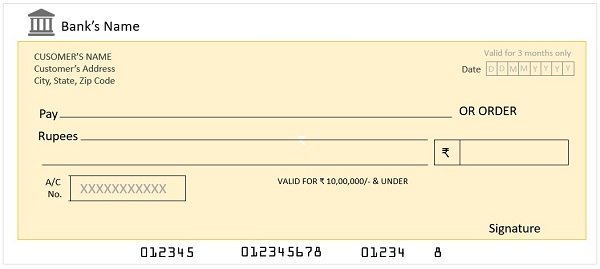

Cheques are issued by the account holders for making different payments. the counterfoils or notes on the cheque book carry details regarding the payment made. It can be used for the purpose of recording transactions. these are deposited together with the pay-in-slip, which can be used as a source document.

Specimen of Cheque

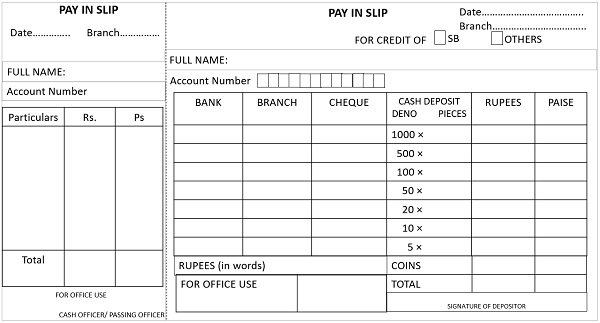

A form is provided by the bank to its customers or account holders at the time of depositing the cash or cheque at the bank.

It is divided into two parts. The part on the left is used as a counterfoil, whereas the right part is for use by the banker. Both the parts are stamped and signed by the cashier when cash or cheque is deposited and the counterfoil is returned to the customer. It contains the details of cash or cheque deposited, name of the bank branch, account number, name of the account holder, the signature of the depositor, cheque number, etc.

Specimen of Pay-in Slip

Apart from the documents given above, there are other documents also which serve as evidence for recording transactions like the point of sales summary, salary slip, bank statements, utility bills, etc.

Source documents act as a piece of objective documentary evidence, on the basis of which business transactions are entered in the books of accounts. They serve as proof that the transaction actually happened. Also, they support the internal control of the organization’s funds and other resources.

Well, the outline of the source document with a brief sample of it… Great thanks to the publication authority…